Table of Contents

In today’s financial landscape, a robust credit score is more than just a number—it’s a gateway to a world of opportunities. From securing a mortgage to obtaining favorable loan terms, your credit score plays a pivotal role in shaping your financial future. Understanding what constitutes a good score, partnered with strategies for improvement, can transform your access to financial products and services. Moreover, with platforms offering a credit score check free of charge and comprehensive insights from score Experian reports, monitoring your financial health has never been easier.

This article will guide you through essential steps to boost your credit score, underscore common mistakes to avoid, and highlight tools and resources that can assist in your journey. From leveraging debt consolidation to benefit your credit report to understanding the nuances between a FICO Score and other score ranges, our goal is to empower you to take control of your financial destiny. Whether you’re conducting a credit score check or seeking to elevate your credit score free of obstacles, this planning guide is designed to pave the way toward the realization of your financial objectives.

Understanding Credit Scores

What is a Credit Score?

A credit score is a numerical expression based on a level analysis of a person’s credit files, to represent the creditworthiness of an individual. Derived from credit report information, a score is essential for lenders to evaluate the risk of lending money . The FICO scoring system, introduced by the Fair Isaac Corporation in 1989, is one of the most commonly used credit scores in the United States. This system evaluates several types of financial information from three major credit bureaus—Experian, Equifax, and TransUnion—each of which may score slightly differently depending on the data they have .

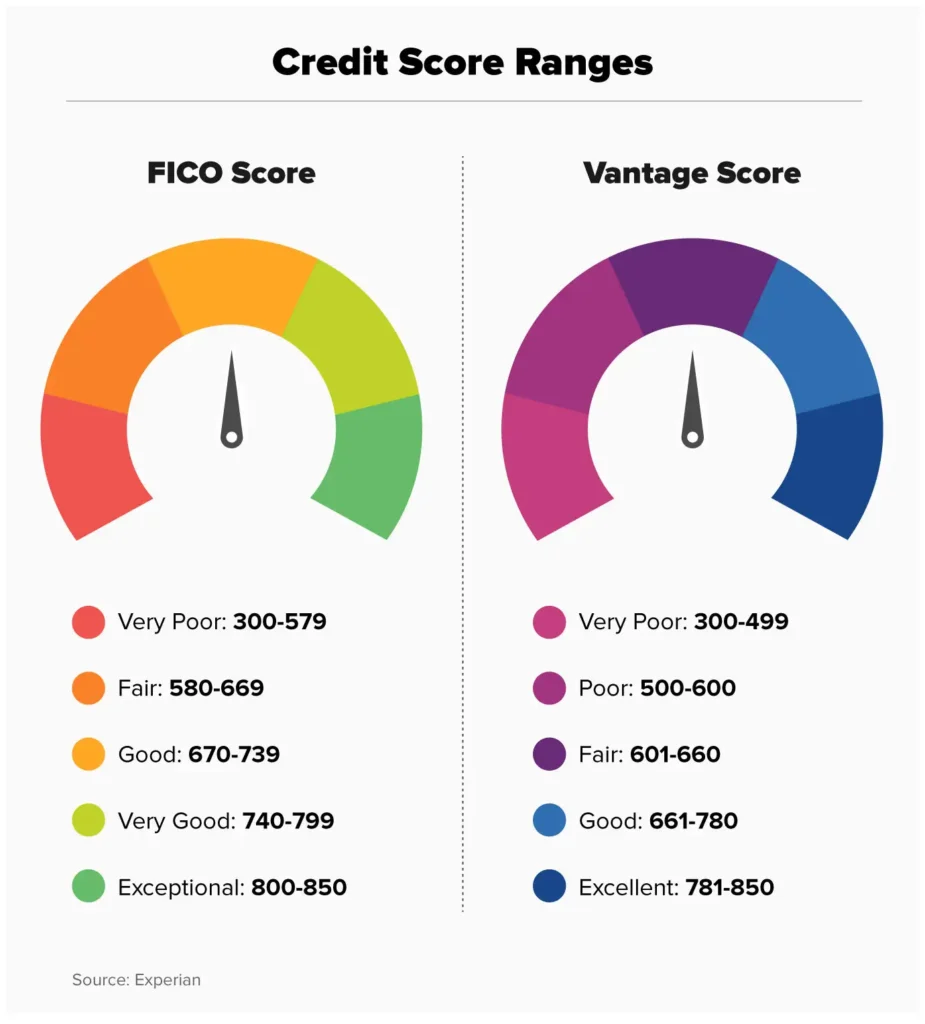

Image featuring two credit score ranges: FICO Score and Vantage Score. Both gauges display color-coded ranges with corresponding labels: Very Poor, Fair, Good, Very Good, and Exceptional for FICO; Very Poor, Poor, Fair, Good, and Excellent for Vantage. The visual clearly breaks down each credit score category. | MONEY6X

Factors Affecting Credit Scores

Credit scores are calculated by considering various elements of an individual’s credit report, including payment history, credit utilization, length of credit history, types of credit used, and recent credit activities. Each of these components is weighted differently in calculating the score. For instance, payment history is the most significant factor, affecting as much as 35% of the FICO Score . Credit utilization, or the amount of credit you are using compared to your available credit limit, also plays a crucial role, accounting for 30% of the score .

Other factors include the length of credit history, which contributes about 15%, and the mix of credit accounts, which affects 10% of the score. New credit inquiries, indicating recent credit applications, also impact the score but to a lesser extent (10%) . These factors are designed to give lenders a comprehensive view of financial behavior, predicting the risk associated with lending.

Importance of a Good Credit Score

Having a good credit score is paramount in securing financial products with favorable terms. A higher score can help individuals obtain better interest rates on loans and credit cards, which translates into lower borrowing costs. For example, a difference in scores can significantly affect the terms of a mortgage, potentially saving a substantial amount in interest payments over the life of the loan .

Moreover, credit scores extend beyond just borrowing terms. They can influence one’s ability to rent an apartment, secure a job, or even negotiate better terms with utility and service providers. In many cases, a good score is seen as indicative of financial reliability and responsibility, which can be beneficial in various aspects of life .

Steps to Boost Your Credit Score

Pay Credit Card Balances Strategically

To enhance one’s credit score, individuals should aim to maintain their credit card balances well below their credit limits. Ideally, keeping utilization under 30% is recommended, but lower percentages can lead to even better scores. Paying down balances before the billing cycle closes ensures the card issuer reports a lower balance to credit bureaus, positively impacting the score .

Ask for Higher Credit Limits

Requesting an increase in credit limits can also improve one’s credit score by lowering the overall credit utilization ratio. If one’s financial situation has improved, such as a higher income or a better credit history, they might be eligible for a higher limit. It’s essential to ensure that this does not lead to increased spending. A soft inquiry for a credit limit increase might not affect the score, but a hard inquiry could have a temporary impact .

Become an Authorized User

Being added as an authorized user on another person’s credit card can be a strategic move for building credit. This approach allows individuals to benefit from the primary holder’s credit history without the legal responsibility for charges. However, it’s crucial to ensure that the primary account holder maintains a good payment history, as any negative records could adversely affect both parties’ scores .

Pay Bills on Time

Consistently paying bills on time is the most effective way to boost a credit score. This includes not only credit card payments but also utilities, rent, and other recurring obligations. Services like Experian Boost can track these payments and include them in the score calculation, provided they are made on time. Late payments can significantly damage one’s score, with the impact increasing with the severity and frequency of late payments .

Common Mistakes to Avoid

Missing Payments

One of the gravest errors individuals can make is missing payments on their credit obligations. Even a single missed payment can significantly impact credit scores, as on-time payments are a major factor affecting creditworthiness . A payment that is more than 30 days late may reduce a credit score by up to 100 points, especially if one previously had unblemished credit . To mitigate this, setting up autopay and payment reminders can be crucial steps in ensuring timely payments and maintaining a healthy score .

Applying for Too Many New Credit Cards

Applying for multiple credit cards within a short timeframe can lead to multiple hard inquiries on one’s credit report, which may lower the credit score temporarily . Each new application can be seen as a risk by creditors, potentially leading to higher interest rates or denial of credit . It is advisable to space out applications and assess the necessity of each new card, especially if one’s credit history is short or consists of few accounts .

Closing Old Credit Credit Accounts

While closing old credit accounts might seem like a tidy way to manage one’s finances, it can have unintended negative effects on credit scores. Closing a credit card can increase the credit utilization ratio and decrease the average age of accounts, both of which play significant roles in credit scoring . If the card has a high annual fee or the benefits are no longer worthwhile, closing it might make sense financially, but one should consider the overall impact on their credit score before doing so . Additionally, it is essential to ensure all balances are paid off or transferred before closing a card to avoid increases in utilization rates and potential fees .

Tools and Resources

Credit Monitoring Services

Credit monitoring services are essential for safeguarding one’s financial information against identity theft and fraud, which has become increasingly common with the rise of online transactions. These services monitor one’s credit report for any new accounts or suspicious activities and alert the individual promptly . Notable services include CreditWise from Capital One and Experian’s free credit monitoring, both of which offer comprehensive monitoring without requiring a credit card for signup . Other services like Aura and PrivacyGuard provide additional features like family plans and dark web scanning, enhancing the protection against identity theft .

Rent-Reporting Services

Rent-reporting services can significantly influence one’s credit score by incorporating rental payment history into credit reports. Services like Esusu and PayYourRent facilitate this by reporting timely rent payments to credit bureaus, potentially boosting credit scores . These services usually require the landlord’s participation and may involve fees, but they can be instrumental for renters looking to improve their credit scores through consistent rent payments .

Financial Planning

Financial planning is crucial for managing money effectively and reducing financial stress. Engaging with a financial advisor or utilizing online platforms can help individuals create a tailored financial plan that addresses personal financial goals and challenges . Tools like robo-advisors and online financial planning services provide accessible options for those seeking professional financial guidance without the traditional costs associated with personal financial advisors .

By leveraging these tools and resources, individuals can enhance their financial literacy, protect their personal information, and potentially improve their credit scores, leading to better financial health and opportunities.

Conclusion

In summary, navigating the intricacies of credit scores and understanding how to enhance them is paramount for anyone looking to solidify their financial foundation. By implementing the strategies discussed, such as paying credit card balances strategically, requesting higher credit limits, becoming an authorized user, and ensuring bills are paid on time, individuals can effectively elevate their credit scores. Simultaneously, avoiding common pitfalls like missing payments, applying for too many new credits simultaneously, and closing old accounts can prevent potential damage to one’s credit health. These actions, coupled with the utilization of valuable tools and resources like credit monitoring services and rent-reporting services, empower individuals to take control of their financial destiny.

The significance of a robust credit score extends beyond merely securing loans with favorable terms; it influences various aspects of financial stability and opportunities in today’s world. As such, the commitment to maintaining and improving one’s credit score is an investment in one’s financial future, offering enhanced access to financial products and services while fostering overall financial well-being. Therefore, individuals are encouraged to adopt a proactive approach towards managing their credit scores, leveraging the insights and recommendations provided in this guide as a roadmap to achieving and sustaining financial health and security.